{kind=link}

What is an HMO?

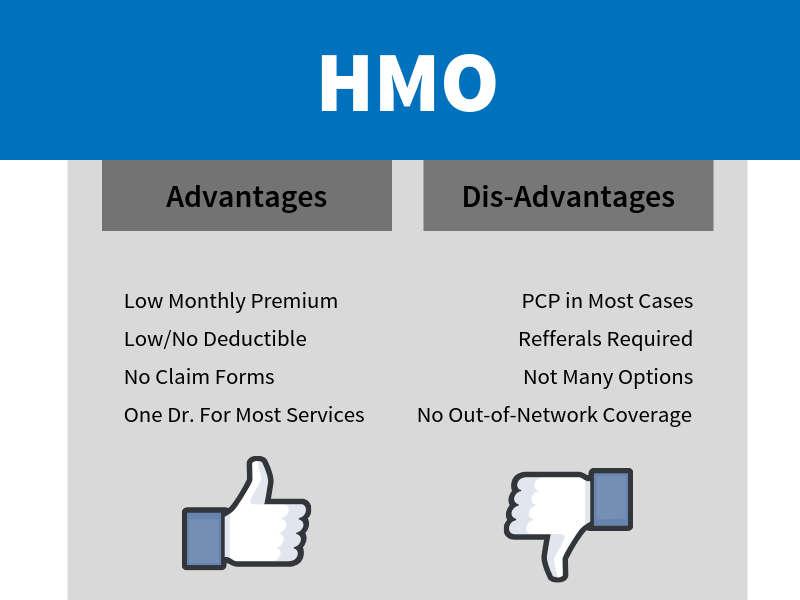

HMO stands for health maintenance organization. They are a medical insurance group that provides health services for a fixed annual fee. There are some benefits as well as some limitations to an HMO health insurance plan. HMO’s have a network of providers and facilities who have agreed to cover certain services at a set pre-determined cost, allowing HMO’s to keep costs in mind for its members.

As the name implies, an HMO’s primary goal it to keep you healthy. They often provide preventative care for a lower copayment or for free, to keep members from contracting something that would be more costly to fix later. HMO’s would rather spend money on wellness benefits to keep you healthy, rather than high bills later due to treating the illness.

Is an HMO health plan right for me?

There are many factors you want to consider when choosing your health insurance plan. The main issues to keep in mind are:

- Monthly Premium

- Out-of-pocket costs

- Using a PCP

- Limited Network Access

- Do I travel?

If you do not require seeing a specialist frequently, you can save money by finding an affordable HMO health plan. With an HMO you will have the least flexibility, but you will have lower costs and easier claims experience than most other health insurance plan types.

How much do HMO’s cost?

In most cases HMO’s have a lower monthly payment than most other insurance plans. They usually also have lower co-pays and coinsurance. HMO’s are great affordable options for those who do not use their insurance too much an do not travel much.

Now while most costs are lower with an HMO, they have no out-of-network coverage unless it’s a true emergency and you will have to choose a PCP.

What is a PCP?

PCP stands for your Primary Care Provider. And as defined by Healthcare.gov it’s a physician, nurse practitioner, clinical nurse specialist or physician assistant, who provides, coordinates or helps a patient access health care services.

In a nutshell your PCP will be your go to doctor. The main doctor who you go to before you can see any other doctor. Before you see a specialist, you will need to get a referral from your PCP. Your PCP is a generalist and responsible for helping you with most of your health care needs. You go to your PCP for your yearly physicals and your preventative care.

If something more serious occurred and you need to see a specialist, your PCP will refer you to a specialist. A specialist could be a psychiatrist, a specialist like a podiatrist, or to a surgeon. Your PCP is kind of like your gate keeper. Before anyone can see you, you must go through him.

Types of Doctors that can be PCP’s

In the U.S. a PCP or primary care provider can be a physician, physician assistant (PA), or a nurse practitioner (NP). Primary Care Physicians are usually a:

- Family Practitioner

- Internal Medicine Doctor

- Pediatrician

- Geriatrician

- OB/GYN

While they are technically specialists, most women see their gynecologist more often than the regular doctor. Due to ACA changes, women are not required to receive a referral to see an OB/GYN. If your current doctor leaves the HMO plan they will notify you and let you choose a new PCP.

HMO Network

With an HMO you must use in network providers. An HMO will have a list of care providers that are in network. If you seek care from a doctor or facility that is out-of-network, your HMO will not pay for it. You will have to pay for the entire bill yourself.

If you’re planning on any medical treatment or procedures, ask questions in advance and ensure that ALL the doctors and nurses providing your care are in network. Believe it or not, just because a lab is down the hall in the same building as your doctor, does not mean that lab is in network for your HMO health plan. Many times, out-of-network providers render care without you even knowing, maybe an anesthesiologist or a surgeon’s assistant. By simply filling a prescription at an out-of-network facility, or getting blood work at the wrong lab, you can easily make a very expensive mistake when you have an HMO plan.

HMO Out-of-network exceptions

In few instances your HMO will allow you to seek out-of-network services and they will still cover them. Those instances are:

- True Emergencies

- HMO does not have an in-network provider for service you need

- You’re in the middle of treatment when you start the HMO and your specialists doesn’t accept the HMO

HMO’s by the Numbers

According to the Henry J Kaiser foundation as of 2016 there were 470 HMO’s health plans available in the United States. California has the most with access to 178 HMO’s. Vermont has the least with only 32 HMO’s available.

As of 2016, around 92 million Americans have HMO health coverage, making it the most popular health insurance network type. That wasn’t always the case. Look back to even just 2014 and PPO’s were the most popular plan type. Now HMO’s are over 50% of the plans chosen while PPO’s are chosen around 20% of the time. The main reason consumers have been choosing HMO’s are their affordability.

Different HMO Plan Types

“Open Access” and “POS” (point of service) plans are a combination of a HMO health plan and a traditional indemnity plan. The members are not required to use a PCP or “gatekeeper” to obtain a referral. In that instance the Indemnity benefits are applied. If they decide to use the PCP to get a referral then the HMO benefits are applied.

*Make sure you pre-arrange the out-of-network care with your HMO and keep them in the loop.

Every plan has its own terms and conditions, so ensure you check the plan outline to understand how your specific plan works or speak to a licensed agent. Ultimately whether a HMO is the right health plan for your or not depends on your specific health needs and budget.